Fed-Favored Inflation Gauge Is Set to Ease to Seven-Month Low

February 23, 2025 | by ltcinsuranceshopper

The Federal Reserve’s preferred inflation metric is expected to cool to the slowest pace since June, but glacial progress on taming price pressures overall will keep policymakers cautious about lowering interest rates further.

Author of the article:

Bloomberg News

Molly Smith and Craig Stirling

Published Feb 22, 2025 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

jggojrinf60(0po1sajj}xd[_media_dl_1.pngBloomberg

Article content

(Bloomberg) — The Federal Reserve’s preferred inflation metric is expected to cool to the slowest pace since June, but glacial progress on taming price pressures overall will keep policymakers cautious about lowering interest rates further.

Article content

Article content

The core personal consumption expenditures price index — which excludes often-volatile food and energy costs — probably rose 2.6% in the year through January in Commerce Department data due on Friday. Overall PCE inflation likely eased on an annual basis as well, according to the median estimate in a Bloomberg survey of economists.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

The decline will probably come from categories that were relatively tame in separate wholesale inflation data that feeds through to the PCE, according to Bloomberg Economics. But components that registered strong increases in the consumer price index will keep the PCE running above the Fed’s 2% target.

That’s a big reason why officials prefer to keep rates on hold for the time being. Michael Barr is due to speak for likely his last time as the central bank’s vice chair for supervision as he prepares to step down at the end of the month, while Richmond Fed President Tom Barkin and Cleveland’s Beth Hammack are among others scheduled to deliver comments.

At the same time as the PCE report, the Commerce Department will release the latest goods-trade balance, which widened to a record in December and will be a key focus for President Donald Trump in his second term. Other data due for release in the coming week include new-home sales, consumer confidence and the government’s second estimate of fourth-quarter growth.

What Bloomberg Economics Says:

“We expect personal-consumption data to show personal spending contracted in January, while core PCE inflation likely slowed to 2.6% year over year. The Trump Trade — a bet on higher inflation – may look increasingly unattractive.”

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

—Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins, economists. For full analysis, click here

In Canada, gross domestic product data for the fourth quarter is likely to show an economy picking up steam following aggressive rate cuts — though that momentum may stall as the looming trade war weighs on business investment.

Elsewhere, Germany’s election, inflation in Australia and the biggest euro-zone economies, and a rate cut in South Korea may be among the highlights.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

Asia

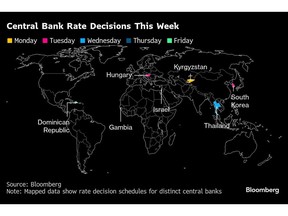

The Bank of Korea will be in the spotlight on Tuesday when authorities decide whether to resume the rate-cut cycle.

While many economists expect the BOK to ease in a bid to prop up domestic demand and get ahead of any tariff impact on exports, Governor Rhee Chang-yong injected uncertainty earlier this month by saying it was by no means a done deal.

The following day, the Bank of Thailand is seen holding its benchmark at 2.25%, though Bloomberg Economics expects pressure to continue for another cut later this year.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Fresh off its first rate cut since 2020, the Reserve Bank of Australia will get consumer inflation data that’s forecast to show price gains accelerated marginally for a third month in January.

Japan publishes CPI data for Tokyo that may show inflation in the capital stayed elevated in February, while Singapore’s core CPI gains probably moderated to 1.5% in January.

Sri Lanka releases CPI statistics on Friday. China reports preliminary PMI data for February on Saturday, with a key being the extent to which the manufacturing gauge recovers after a lunar-holiday dip in January. Bloomberg Economics expects the data to reinforce the case for policy support.

Taiwan reports preliminary gross domestic product figures for the fourth quarter on Wednesday, and trade data are due during the week from the Philippines, South Korea, Sri Lanka, Thailand and Hong Kong.

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

The aftermath of Sunday’s election in Germany will be the focus for investors. The pro-business CDU/CSU bloc, led by Friedrich Merz, is expected to take the biggest vote share after a campaign that often dwelled upon the country’s dismal economic record under Chancellor Olaf Scholz.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Recent upticks in investor confidence and among purchasing managers likely came to late to help the incumbent. Similarly, the closely-watched Ifo business sentiment report on Monday is expected to show the highest reading since October.

One of the main questions following the snap ballot will be the future of Germany’s so-called debt brake, a topic that’s preoccupied Bundesbank President Joachim Nagel for some time.

Reporters may quiz Nagel on that topic when he presents his institution’s annual report on Tuesday. He’s also likely to use the opportunity to comment on the European Central Bank’s next steps. A pre-meeting quiet period will then begin before the March 6 decision.

Data that may draw attention in the euro region in the coming week include inflation on Thursday and Friday from its four biggest economies, with economists anticipating outcomes ranging from slowing in Germany and France to a stable outcome in Spain and an uptick in Italy.

In the UK, meanwhile, several speeches by Bank of England policymakers are scheduled, including Deputy Governors Clare Lombardelli and Dave Ramsden.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Elsewhere in Europe, Swedish, Czech and Icelandic gross domestic product numbers for the fourth quarter will be released.

In South Africa, data on Wednesday will likely show inflation quickened to 3.2% in January from 3% a month earlier. The reading will be the first since the nation’s consumer price index was overhauled. The release was delayed by a week to allow the statistics agency to conduct additional checks and verifications on the data.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

On Wednesday and Thursday, South Africa will host the first Group of 20 finance minister-central bankers summit since Trump returned to office. The meeting comes as the global economy enters a precarious phase, with markets shaky and the easing cycle at risk because of US protectionist polices.

It’s also being overshadowed by the US leader’s public spat with President Cyril Ramaphosa over domestic land laws, equality policies and Israel’s war on Gaza. Treasury Secretary Scott Bessent has pulled out of the event.

Two key monetary decisions in the wider region will draw investors’ attention:

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Israel’s central bank is set to hold its base rate at 4.5% for a ninth straight meeting on Monday. Ceasefires with Hamas in Gaza and Hezbollah in Lebanon have started to lessen economic pressures, but inflation is still at 3.8%, above the country’s official target of 1%-3%. Governor Amir Yaron has pointed to that and signaled easing won’t begin until the second half.

Hungary’s central bank is expected to keep interest rates stable for a fifth month on Tuesday at the final meeting to be chaired by outgoing Governor Gyorgy Matolcsy. Policymakers have no room to cut borrowing costs this year, another outgoing official, Gyula Pleschinger, told Bloomberg in an interview.

Latin America

Mexico’s mid-month consumer prices report may serve up a dose of whiplash, with the early consensus for a jump back up of some 30 basis points from 3.48% in the second half of January.

Less alarming, the core print may only budge slightly from its current 3.61%, within the central bank’s 2% to 4% inflation tolerance range though above the 3% target.

Latin America’s No. 2 economy will also serve up the January’s unemployment rate — currently running near all-time lows — along with trade, lending and current account data.

Advertisement 8

This advertisement has not loaded yet, but your article continues below.

Article content

Chile’s end-of-month data dump for January, which comprises six separate indicators including industrial production, retail sales, copper output, should show little drop-off from the economy’s strong finish to 2024.

Argentina closes the books on 2024 with December GDP-proxy readings. After pulling out of recession and posting two months of better-than-expected growth, the nation may lead growth among the region’s big economies in 2025.

A smattering of Brazilian economic reports for December posted earlier this month, including Brazil GDP-proxy data and retail sales, suggest Latin America’s biggest economy may finally be cooling off.

Along those lines, national unemployment figures for January should show a second month of weakening of the economy’s tight labor market.

On the other hand, consumer prices can be expected to rebound from last month’s 4.5% reading — the top of the central bank’s tolerance range — and may not return there before some time next year.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Brian Fowler, Laura Dhillon Kane, Monique Vanek, Ott Ummelas, Paul Wallace, Piotr Skolimowski and Robert Jameson.

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

1 minute

_gac_

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests