Why your financial adviser wants you to take more risk than you think you can handle

September 18, 2025 | by ltcinsuranceshopper

Your financial adviser may be pushing for a higher stock allocation than feels right to you. Before you dismiss that advice – or switch advisers – new research suggests this tension may actually work in your favor.

“Market risk is a crucial consideration for people relying on financial assets as a major source of support in retirement,” wrote Jean-Pierre Aubry and Yimeng Yin, authors of a new paper from the Center for Retirement Research at Boston College.

“Retirement investors often have misperceptions about asset returns and limited knowledge about financial markets, potentially jeopardizing their long-term security.”

In What Stock Allocations Do Advisors Suggest and Does It Impact Clients? the researchers found that advisers’ recommended stock allocations often exceed what investors say they want. For example, retirees with average risk preference typically favor about 39% in stocks. Advisers, in contrast, recommend closer to 48%.

That nine-point gap isn’t trivial — it reflects a fundamental divide in how retirement investing should be approached. And the study suggests the gap may also be influenced by compensation. Advisers who earn a higher share of their fees from assets under management tend to recommend more aggressive stock allocations.

Still, Aubry and Yin conclude that higher equity exposure is “likely beneficial for many investors” because advisers bring a more realistic view of long-term risks and returns — even if the incentives align with their own fees.

Source: TheStreet

Good financial advisers focus on more than market risk

Some planners, however, argue the research frames the conversation too narrowly.

Ben Bolen, a certified financial planner with University Investment Services, said retirees often focus too much on market swings while underestimating two equally serious threats: inflation and longevity.

“Reducing market exposure may help someone feel good in the short term,” Bolen said, “but planners have to ensure their clients actually do good over the long term.”

Related: Latest inflation data resets Social Security COLA outlook for 2026

He points to strategies such as the bucket approach – dividing assets into near-term cash reserves and long-term growth pools – as a way to balance immediate spending needs with the need to keep pace with rising costs over decades.

In his view, a thorough adviser goes well beyond a five-question “risk tolerance” survey. They evaluate multiple risks – market, inflation, and longevity – and design allocations that reflect not only numbers on a page but also the client’s real-life goals, needs, and concerns.

Others agree. “Risk tolerance is dependent on the client, bottom line,” said Kyle Playford, a certified financial planner with Freedom Financial Partners. He added that both preference and capacity can shift over time and should be reviewed at least annually. “Showing the impact of higher return assumptions in financial plans can help clients see the power of investing in stocks versus bonds.”

Risk preference vs. risk capacity: why the difference matters for investors

Patrick Huey, a certified financial planner with Victory Independent Planning, believes the Center for Retirement Research report “strikes at the heart of an essential planning issue: Should advisers recommend stock allocations based on what clients want – their risk preference – or what they can truly afford to risk – their risk capacity?”

In Huey’s view, risk preference is how much market risk an investor feels comfortable taking. It’s subjective, shaped by personality, past experiences, and even the latest headlines – and it can shift wildly with each market cycle.

Risk capacity, by contrast, is objective. It measures how much risk someone can and should take given their time horizon, spending needs, other assets, and guaranteed income. It’s about facts, not feelings.

Related: White House makes risky changes to retirement accounts

“Many older investors are too pessimistic about stocks,” Huey said. “Left to their own preferences, they’d likely go too conservative. Advisers who ground their guidance in a client’s financial reality – risk capacity – are doing them a favor, ensuring growth potential matches longevity, inflation risk, and future needs.”

To bridge the gap, Huey uses a quantitative, multi-scoring framework. “We deliberately separate and measure both risk preference and risk capacity, then compare those to the actual risk in the portfolio,” he said. “By quantifying each dimension, we can have more substantive conversations – and show clients how a small increase in equity exposure might protect their lifestyle longer.”

Huey calls this balance between numbers and behavior the art and science of retirement planning.

Two schools of thought among financial advisers

From there, financial planners tend to fall into two broad camps.

The “mathematical realist” approach to investment advising

Mathematical realists argue that investors need to be nudged beyond their comfort zones because:

- Inflation and longevity risks often outweigh market risk.

- An 80/20 stock-bond portfolio can cover years of retirement withdrawals from the bond side alone.

- Emotional preferences often lead to underfunded portfolios that can’t support 30 years of retirement.

Tyson Sprick, a certified financial planner with Caliber Wealth Management, makes that last point concrete. “In general, I would say that investors tend to get more conservative than is really necessary, even in retirement,” he said.

Sprick breaks portfolios down into years of income. “If we are taking around 4% a year from the portfolio, an 80/20 stock/bond allocation, which many would consider too aggressive, covers five full years of distributions without even touching the equity side. This framework typically gives the client a little more peace of mind and comfort in leaving the majority of their portfolio to continue to grow.”

Related: One Big Beautiful Bill Act makes Roth IRA conversions more complicated

Catherine Valega, a financial planner with Green Bee Advisory, emphasizes that allocation decisions should be driven by the financial plan, not the other way around.

“One investor’s allocation depends on their financial plan,” she said. “We can’t invest until we know how to invest. If a client still needs growth, I like to keep at least 80% in stocks. If they don’t need growth, we can invest more conservatively. You can’t create an allocation before knowing long-term goals, income, and assets.”

The “behavioral pragmatist” approach to investment advising

Behavioral pragmatists counter that pushing clients too far backfires. They argue that:

- Aggressive allocations trigger panic selling during downturns.

- Accepting lower returns is better than enduring behavioral mistakes.

- Sustainable allocations beat “optimal” allocations that clients can’t stick with.

For Kassi Fetters, a certified financial planner with Artica Financial Services, the solution is collaboration. “The most important steps I can take as an advisor are to make sure the client understands what they are invested in and to create a portfolio the client is comfortable holding over the long term,” she said.

Related: Social Security COLA for 2026: What Retirees Can Expect

That means respecting a client’s choice – even if it results in lower returns. “If a client wants a conservative portfolio and understands their return may be less over the long run, which will affect how much they can draw, then why push them?” she asked. “Why create stress and sleepless nights for clients by pushing for aggressive allocations that they’ll want to sell when markets go down?”

For Fetters, portfolio allocation should be a collaborative process, not a top-down prescription.

“Pushing a client into a more aggressive portfolio may increase returns; however, it will have negative ramifications when there’s negative market news and the client wants to move into a more conservative portfolio,” she said. “This creates exactly what we don’t want — selling in a down market instead of holding.”

Beyond the stock/bond investing framework

Some advisers go even further, questioning whether the stock/bond framework itself is the right starting point.

Keith Schnelle, a certified financial planner with Solutia Globa, says the more useful discussion isn’t about the exact percentage in stocks but about how much of a household’s wealth should be held in liquid securities at all.

Schnelle contends that many advisers reduce portfolio design to dividing money among stock-based mutual funds and ETFs. In his view, true diversification requires more: balancing liquid and illiquid investments, tangible and intangible, domestic and foreign.

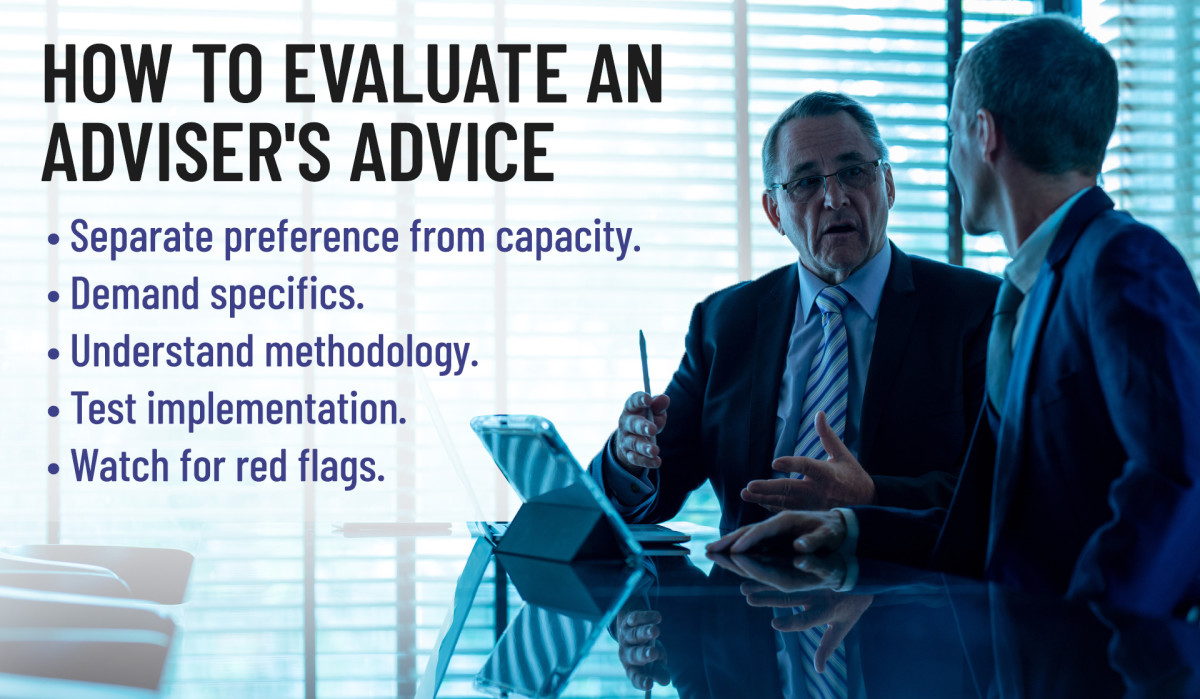

How retirement investors can evaluate their financial advisers

Rather than simply accepting or rejecting your financial adviser’s recommendations, use this framework to evaluate their advice:

- Separate preference from capacity. Your comfort level matters, but so does what your finances can actually support. Both must be measured.

- Demand specifics. Ask for projections comparing conservative and aggressive allocations, depletion probabilities, and the role of Social Security and pensions.

- Understand methodology. Ask how they distinguish preference from capacity, what strategy they use (total return, bucket, floor, and upside), and how compensation may influence their advice.

- Test implementation. See whether they use tools like bucket strategies or income floors to make higher allocations psychologically sustainable.

- Watch for red flags. If your adviser can’t explain their process beyond a generic questionnaire, that’s a problem.

Ultimately, the goal isn’t to find the “perfect” allocation, but one that balances mathematical soundness with behavioral sustainability. The Center for Retirement Research study suggests that some tension between adviser recommendations and client preferences is normal — and may even be healthy.

But for that tension to be productive, advisers must do more than push numbers. They need to explain their reasoning clearly, implement their advice in ways clients can stick with, and revisit the plan as circumstances change.

If your adviser can’t do that, the problem isn’t the allocation — it’s the advisory process.

Related: Medicare beneficiaries quietly face looming crisis

RELATED POSTS

View all

Horizon Bien-être Edition Spéciale: Le Secret de l’Huile de Coco Révélé

March 12, 2025 | by ltcinsuranceshopper

NIO Stock Hits 52-Week High as Analysts Boost Targets

September 29, 2025 | by ltcinsuranceshopper