Nasdaq Sell-Off: 2 Stocks Down 53% and 31% to Buy on the Dip and Hold Forever

March 14, 2025 | by ltcinsuranceshopper

The Nasdaq Composite has dropped roughly 13% in less than a month (as of this writing). As distressing as it feels, long-term investors must remember that 10% “corrections” in the market are surprisingly common — typically occurring once every two years.

These corrections are the price we pay to take part in an investing process that could lead to our financial independence. As author Morgan Housel beautifully summed up: “Volatility is [the] price of admission. The prize inside [is] superior longterm returns. You have to pay the price to get the returns. Many aren’t.”

The silver lining to any good stock market sell-off is that many great companies become discounted, which is ultimately a long-term opportunity for those willing to pay the price of admission. Here are two of my favorite Nasdaq stocks to buy amid the current turmoil and hold for decades.

1. The Trade Desk: Down 53% from 2025 highs

Standing in stark contrast to the “walled gardens” of Meta Platforms, Amazon, and Alphabet, The Trade Desk (TTD -10.50%) — with its omnichannel, ad-buying platform — leads the way on the open internet.

The Trade Desk connects ad agencies and their branded customers with publishers on its platform, offering an alternative to the walled garden providers that typically face numerous conflicts of interest. This objectivity from The Trade Desk’s independent demand-side platform — and its leadership position in the niche — have proven to be among the company’s most powerful traits and have helped power its stock 20 times higher since 2016.

However, after The Trade Desk reported earnings in February that didn’t meet its own expectations for the first time in 33 straight quarters, the stock lost over one-third of its value overnight. Since then, it has slid further amid the Nasdaq sell-off, and its shares sit 53% below their 2025 highs.

So, why am I looking to add to my shares in The Trade Desk right now?

First, the company is in the midst of switching customers from its old Solimar platform to its new, AI-powered Kokai system. Since The Trade Desk is currently maintaining both platforms until all of its customers switch to Kokai by the end of 2025, its growth attack has temporarily taken a backseat.

Second, though its 22% sales growth in the fourth quarter missed expectations, The Trade Desk doubled the growth rate of the global advertising industry in 2024. Management is guiding for 17% sales growth in the first quarter, which compares nicely to GroupM’s expectations for the advertising industry to grow by 8% in 2025.

Simply put, I think cutting The Trade Desk’s value in half over 90 days’ worth of sales is harsh, especially as the company is still rapidly gaining market share. Finally, The Trade Desk trades at one of its most attractive valuations of the last decade, following its dramatic pullback.

TTD Earnings and FCF Yields data by YCharts.

Currently, its earnings yield and free cash flow (FCF) yield (the inverse of price-to-earnings and price-to-FCF ratios, so higher is cheaper) are well above historical levels.

Despite being the leading demand-side platform outside of the walled gardens, The Trade Desk only accounts for roughly 1% of the $1 trillion global advertising industry, leaving a massive remaining growth runway.

Connected television, premium video, streaming audio, and international expansion combine to create an array of megatrends that could push The Trade Desk back to new highs, making it a fantastic investment during the Nasdaq sell-off.

2. Wingstop: Down 31% from 2025 highs

Whereas The Trade Desk got throttled for not maintaining its 33-quarter streak of beating expectations, fast-casual chicken wing chain Wingstop (WING -3.25%) was pummeled by the market even though it extended a streak of its own.

Despite delivering its 21st consecutive year of same-store sales growth, Wingstop saw its shares slide 20% after earnings in February and now sits 31% below its 2025 highs. After the company slightly missed analysts’ sales expectations for Q4, the market has essentially reduced Wingstop’s market capitalization from $9 billion to $6 billion because it was $3 million short in sales during the quarter.

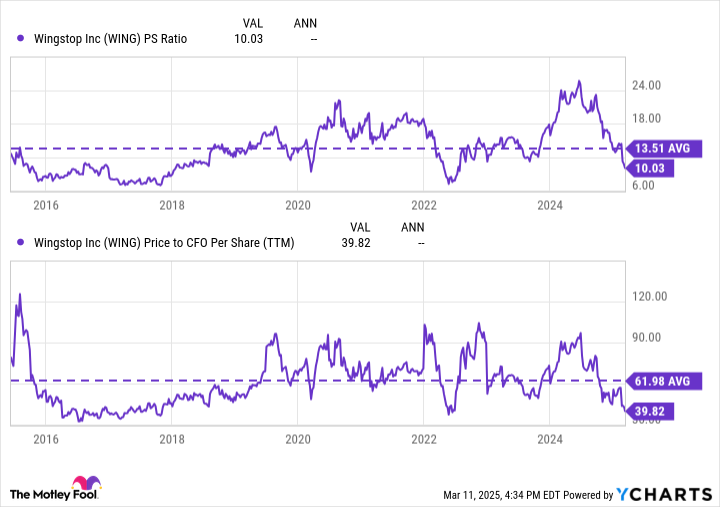

In my opinion, this is an overreaction and makes the quickly growing franchisor an appetizing buy. Following its 31% decline in share price, Wingstop trades near what I would argue is a once-in-a-decade valuation.

WING P/S and P/CFO Ratio data by YCharts. P/S = price-to-sales.

While these figures are lofty compared to most S&P 500 stocks, Wingstop may deserve this premium as it still has a long growth runway ahead of it. The company currently has 2,550 stores, and Wingstop’s management believes it can roughly quadruple its store count over the long term.

The company grew its store count by 16% in 2024 and expects to see similar marks in 2025 — all while increasing its same-store sales by mid- to high-single digits this year. With 2,000 restaurant commitments under development agreements, Wingstop’s pipeline for new locations nearly outweighs its existing store count.

Combine this growth potential with the company’s recently discounted price and its 0.5% dividend yield (whose payments have nearly quadrupled in just seven years), and I believe Wingstop is a top Nasdaq stock to buy on the dip and hold forever.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Josh Kohn-Lindquist has positions in Alphabet, The Trade Desk, and Wingstop. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and The Trade Desk. The Motley Fool recommends Wingstop. The Motley Fool has a disclosure policy.

RELATED POSTS

View all

Singapore buys only small amount of Nvidia chips, official says

February 18, 2025 | by ltcinsuranceshopper

How Scholz’s party is losing ground in Germany’s industrial heartland

February 21, 2025 | by ltcinsuranceshopper

Billionaire Ray Dalio's blunt message on economy turns heads

March 6, 2025 | by ltcinsuranceshopper