Have $500? 2 Absurdly Cheap Stocks Long-Term Investors Should Buy Right Now

By ltcinsuranceshopper

March 16, 2025

With the recent market sell-off, a number of stocks have just been tossed right into the bargain bin. This includes some very well-known names that are trading at very low valuations.

Let’s look at two absurdly cheap stocks to buy right now.

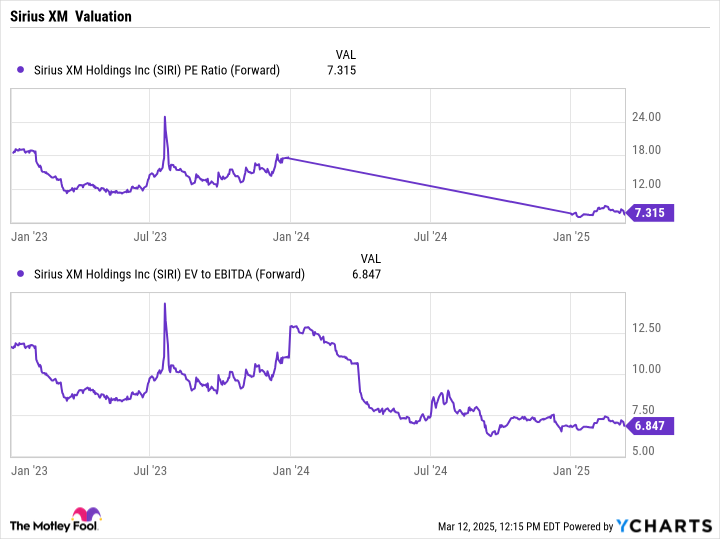

For those unfamiliar with Sirius XM (NASDAQ: SIRI), it operates a satellite radio service. It also owns the Pandora streaming music app and a podcast network. The company became fully independent last year following a complicated spinoff/reverse stock-split transaction with Liberty Live Group.

While not a growth stock, the one thing the stock is today is cheap.

It currently trades at a forward price-to-earnings (P/E) ratio of less than 7.5 times based on 2025 analyst estimates and an enterprise value (EV)-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio of below 7 times. The latter metric takes into consideration its net debt as well as takes out the non-cash depreciation from its capital expenditures (capex) used to launch satellites that is reflected in that debt. EV/EBITDA gives a better picture of Sirius XM’s current operations, although the stock is still cheap by either valuation metric.

While Sirius XM isn’t suddenly going to be confused for a growth stock, it does have a number of avenues to bolster its stock price. One of the biggest opportunities for the company is deleveraging and reducing its debt. At year-end, the satellite radio operator carried about $10.3 billion in debt on its balance sheet.

While the company isn’t growing its revenue, one thing it does do is generate a lot of free cash flow. In 2024, it produced free cash flow of $1 billion, and it projected $1.15 billion in free cash flow this year. Those numbers, meanwhile, should continue to rise over the next few years as its satellite-related capex will continue to decline. It will go from around $220 million this year to only $95 million in 2026 and to nearly $0 by 2028.

Below is Sirius’s XM’s satellite-related capex spending plan.

2024

2025

2026

2027

2028

Satellite capex

$220 million

$95 million

$45 million

$0 million

Data source: Sirius XM presentation.

This should allow the company to meaningfully reduce its debt over the next five years, which should help boost its stock price.

Meanwhile, after reducing costs by $350 million in 2023 and 2024, the company is looking for an additional $200 million in cost savings this year. This is coming from optimizing market spend and reducing operating expenses.

In addition, the company is reworking how it prices and markets its subscriptions this year. It will shorten the length of introductory offers for automotive trials while offering new lower-priced package options that start at about $10 a month. It will also offer additional add-ons for things such as talk and sports radio. It expects this to have an impact on its first-half results but then lead to better results going forward through higher customer satisfaction.

Overall, these cost reductions and its customer retention strategy should help lead to a higher stock price over the long term.

Image source: Getty Images

Another stock that has been thrown into the bargain bin is Crocs(NASDAQ: CROX). The company designs and sells its Crocs brand footwear, which is best known for its classic molded clog silhouette. It also owns the HeyDude footwear brand, which offers casual shoes with a flex-and-fold outsole. Crocs acquired the brand in 2022.

Crocs’ namesake brand has been performing well, with growth being led by expansion into international markets and the introduction of new silhouettes such as sandals. Last quarter, the Crocs brand saw revenue rise 4% to $762 million, with international sales climbing 11.5% to $291 million.

However, the HeyDude brand has been an issue. While the brand was growing fast, it wasn’t being managed properly and Crocs overshipped the product into the wholesale channel, which led to heavy discounting of older product in some online channels. The company then went on to clean up its distribution by removing many retail accounts.

These troubles were seen in Crocs’ results through the first three quarters of 2024 when HeyDude sales fell by more than 17% each quarter. However, the company did see some strong signs of progress in turning the brand around in Q4, when HeyDude sales came in flattish year over year.

The company credited the use of celebrity endorsers, including Sydney Sweeney, in helping improve the brand’s identity. It also noted that its strategy to begin marketing to younger females was paying off, with new female customers ages 18 to 24 years old growing 160% in the quarter.

While more work needs to be done, this is nice progress. At the same time, turning around HeyDude is the biggest opportunity in front of the company, and successfully doing so would be a big boost to a very cheap stock.

The stock currently trades at a forward P/E of less than 8 times 2025 analyst estimates.

For a solid, well-established footwear brand like Crocs that has continued international expansion opportunities and is seeing progress turning around the HeyDude brand, the company’s valuation is far too cheap at current levels.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $299,728!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $39,754!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $480,061!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

March 16, 2025

March 16, 2025